Nuclear imaging equipment is considered to be a critical advancement in the field of diagnostic imaging techniques. Used to visualise organs that cannot be easily viewed by conventional X-ray systems, these devices are helpful in, for example, bone scans and cardiac scans, but with advancing technologies and hybrid modalities the applications of this equipment have been enhanced.

There are two categories in nuclear imaging equipment: single-photon emission computed tomography (SPECT) and positron emission tomography (PET). Nowadays, both are used for the early diagnosis of Alzheimer’s disease, tumours and for thyroid scans.

Go deeper with GlobalData

The technology in the equipment involves the use of radioactive isotopes, and the resulting radiation is recorded as images and can also be superimposed onto images obtained from other diagnostic imaging techniques, such as computed tomography.

Growing market for nuclear imaging equipment

The global nuclear imaging equipment market was estimated to be worth $1.8 billion in 2010 and is expected to grow at a compound annual growth rate (CAGR) of 7% to reach $2.9 billion by 2017, driven by the increasing applications of these systems in diagnosing oncological and neurological disorders in their early stages. The shift from stand-alone systems to combined modalities has provided physicians with more accurate, clear and precise images, which will increase the demand for nuclear imaging equipment.

The US is the biggest market for nuclear imaging equipment, accounting for 47% of the global total in 2010 (see Figure 1). Valued at $834 million in 2010, it is forecast to grow by 5% annually between 2010 and 2017 to reach $1.2 billion. The major growth drivers in the US are the increasing use of these systems for the early detection of diseases such as cancer and Alzheimer’s, and increased PET and SPECT coverage by the Centers for Medicare and Medicaid Services (CMS).

See Also:

In 2010, GE Healthcare, Philips Healthcare and Siemens Healthcare were the top players in the global nuclear imaging equipment market, with a combined share of 88% (see Figure 2). The market is dominated by these three players due to their global reach, renowned brand names and technologically advanced products.

How well do you really know your competitors?

Access the most comprehensive Company Profiles on the market, powered by GlobalData. Save hours of research. Gain competitive edge.

Thank you!

Your download email will arrive shortly

Not ready to buy yet? Download a free sample

We are confident about the unique quality of our Company Profiles. However, we want you to make the most beneficial decision for your business, so we offer a free sample that you can download by submitting the below form

By GlobalDataMore procedures involving nuclear imaging scans

Figure 3 depicts the growing number of procedures involving nuclear imaging scans due to the higher sensitivity, efficiency and resolution of the imaging equipment, which helps physicians to better understand several diseases. Nuclear imaging scans – being non-invasive and offering a level of detail of diseases unachievable by other imaging procedures, such as X-rays and CT scans – are expected to find increased acceptance from physicians. They not only facilitate more accurate diagnoses and treatments, but also help to keep down healthcare costs by enabling the early detection of various conditions.

Improved technology has made PET systems a preferred choice for the diagnosis and treatment of diseases such as Alzheimer’s, as well as various other cardiovascular and oncological diseases. According to a recent paper, ‘Positron emission tomography imaging of cancer biology: current status and future prospects’, published in Seminars in Oncology by Kai Chen and Xiaoyuan Chen, PET systems are more advantageous than traditional diagnostic imaging techniques. The different stages of a cancer’s development and the post-treatment changes in the patient’s body can easily be visualised, characterised and measured with PET imaging systems. Moreover, PET scans may remove the need for a surgical biopsy.

In 2010, the CMS approved PET scan reimbursement for Alzheimer’s disease, which is expected to enhance the demand for PET systems in the US. PET systems help in diagnosing Alzheimer’s disease early in the disease process stage and also help in differentiating the disease from other neurological brain diseases.

Market restraints

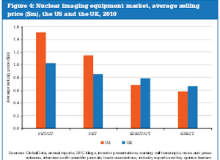

The initial investment required for the installation of nuclear imaging equipment is significant. For example, the cost of a PET/CT system is about $1.5 million in the US and $1 million in the UK (see Figure 4). The cost is high because of the incorporation of CT technology and the use of radioisotopes for diagnosis. Due to the expensive nature of these systems, healthcare facilities such as hospitals and diagnostic centres have been reluctant to invest in them.

Healthcare facilities that purchase medical devices such as PET and SPECT systems often rely on third-party payers such as Medicare, Medicaid or private health insurance plans to reimburse the cost of the diagnostic, screening and therapeutic procedures performed with these devices. In January 2010, the CMS implemented a cut of 36% to nuclear imaging scans reimbursement. This was reduced in May 2010 to 20%.

In November 2010, the CMS announced the reduction of reimbursement for cardiac PET scans by 23%, as a part of its final rule for the Hospital Outpatient Prospective Payment System (HOPPS) and Ambulatory Surgical Center (ASC) services, which became effective in January 2011. Nuclear imaging scanning reimbursement plans available in the US are transparent and cover almost all diseases that require a PET or SPECT scan. However, continuous cuts are affecting patient access to high-quality, cost-effective imaging and diagnostic services, which is negatively affecting the nuclear imaging market.

Radioactive shortages

SPECT imaging primarily uses the radioisotope technetium-99m (Tc-99m) for around 80% of its diagnostic applications. Tc-99m is mainly used for the diagnosis of all cardiac diseases. SPECT consumes a greater number of radioactive tracers compared with PET imaging due to the fact that the primary tracer used for SPECT imaging, Tc-99m, has a long decay life when compared to that of PET imaging, which prevents the tracer from being inventoried for future use. Additionally, PET imaging is faster, which enables PET scans to use low doses of tracers.

There are also supply side pressures for SPECT imaging. The supply of Tc-99m has already been affected by the repeated shutdown of Canada’s aging Chalk River nuclear reactor that produces molybdenum-99 (Mo-99) from which Tc-99m is produced. This facility meets almost 80% of the world’s total requirement for Tc-99m, while the US imports around 50-60% of its Tc-99m from Canada. There are only five other sources in the world accounting for the remaining production of Tc-99m.

The solution seems to be to find alternatives that can secure the supply of Tc-99m or, otherwise, opt for other medical imaging techniques, and PET/CT systems will replace SPECT systems if alternative sources for radioisotopes are not identified in the near future. Meanwhile, GE Healthcare opened its own dedicated PET tracer production facility in 2005 to build confidence in PET/CT systems as well as to secure the supply of radioisotopes for them.